Cash Access Oasis or Desert?

14th November 2019

Despite our preference for digital payments, 97% of us carry cash. In fact, the average amount is £41! This culminated in 2.4 billion ATM cash withdrawals in 2018, totalling £193 billion. It is no wonder then that a recent UK public opinion poll concluded only 36% of UK adults believed they could cope with going completely cashless. Government advisors are concerned too. They state eight million UK adults (17% of the UK population) would get left behind – just think about the number of cash-in-hand employments: window cleaners, gardeners, labourers, to name a few. Additionally, consumer association Which? fears that deprived neighbourhoods have the least access to cash, even though they are more dependent on it than their affluent counterparts. Thus, it seems the concerns about the so-called ‘Cash Deserts’ are justified, at least for the next 15 years anyway.

In response, LINK – the network that connects the UK’s cash machines and enables universal access to people’s cash – has set up a £1 million fund to pay for 40 to 50 ATM’s requested by residents in the ‘Cash Deserts’. To qualify as a ‘Cash Desert’, areas must not have access to a free to use ATM or Post Office within 1km and the machine must be in a secure locale.

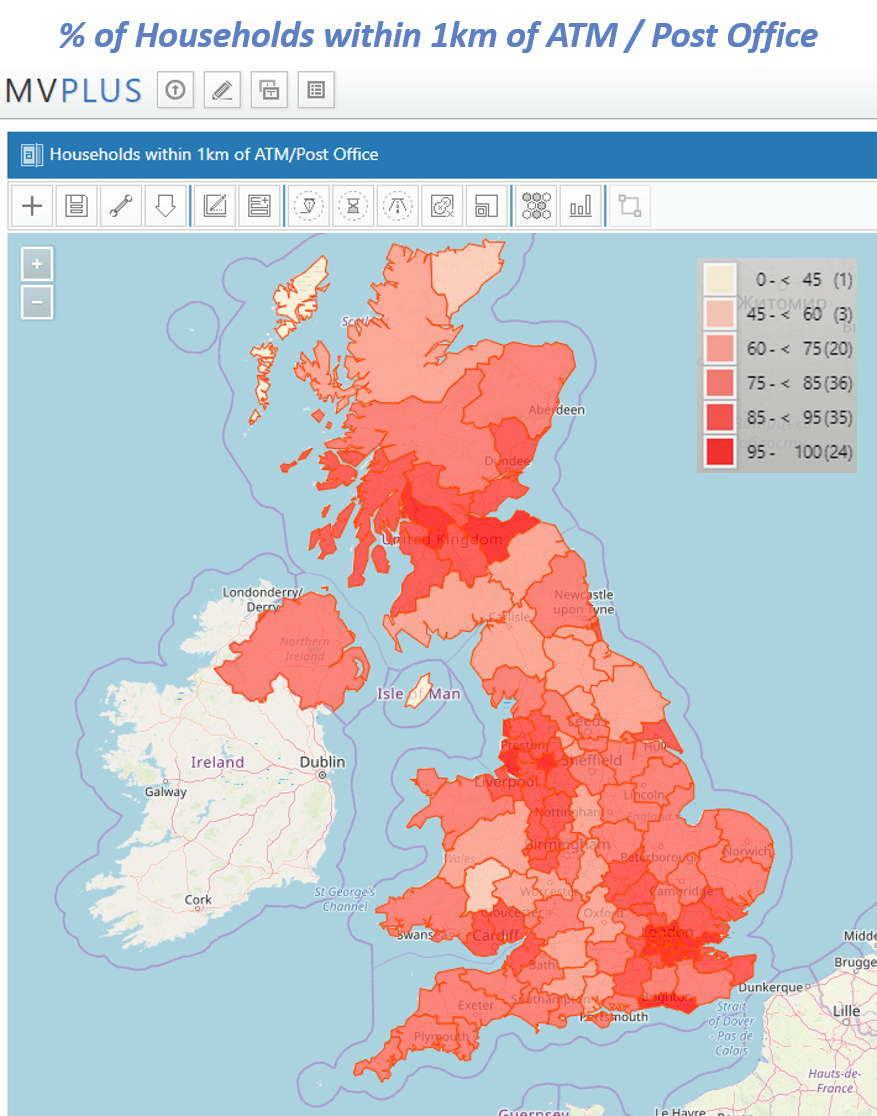

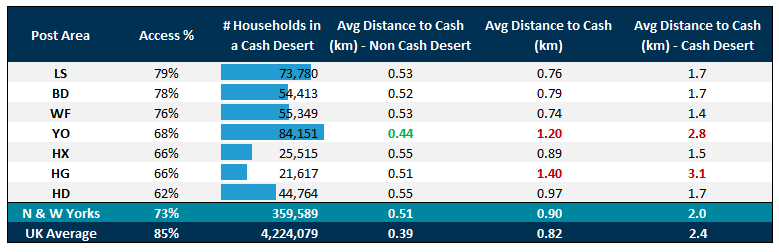

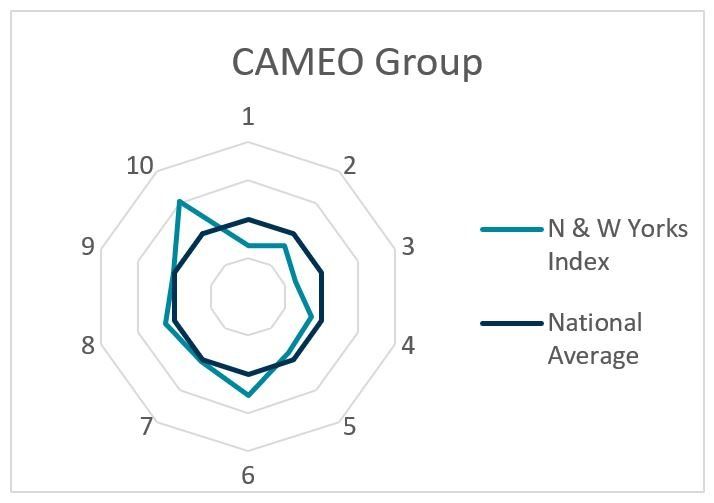

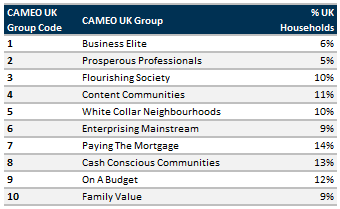

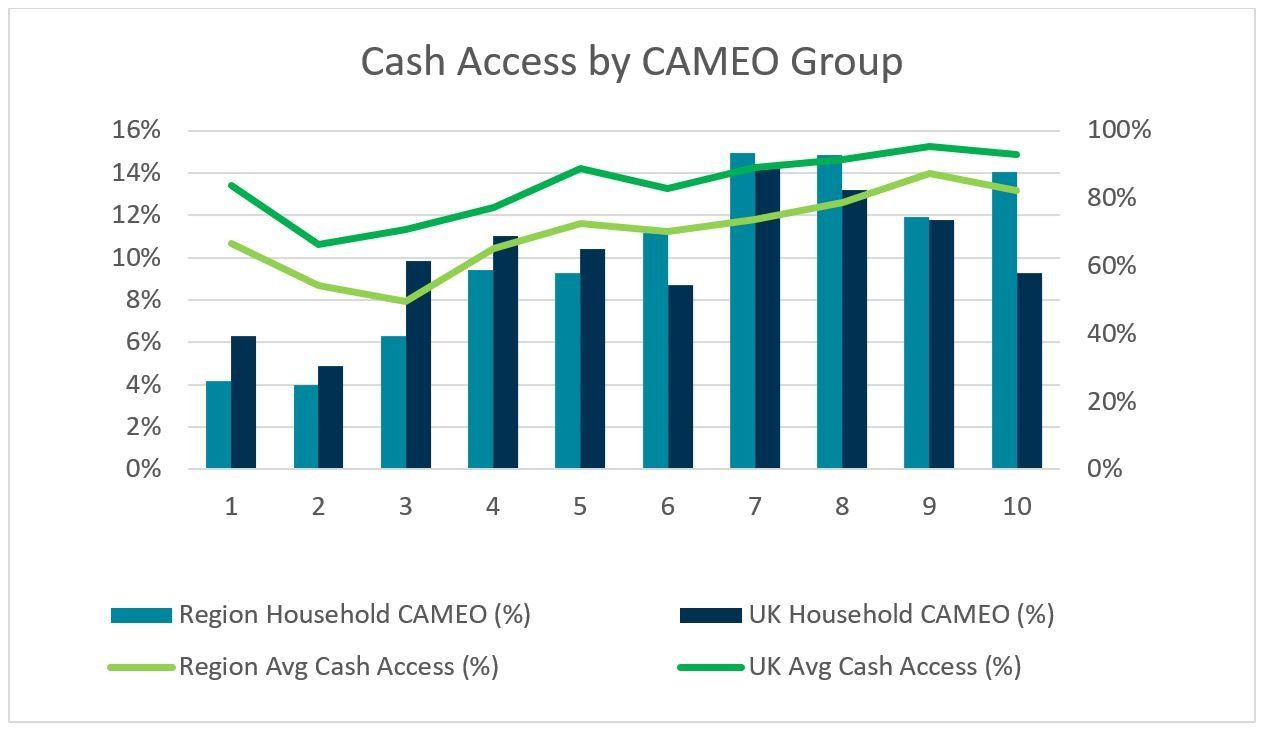

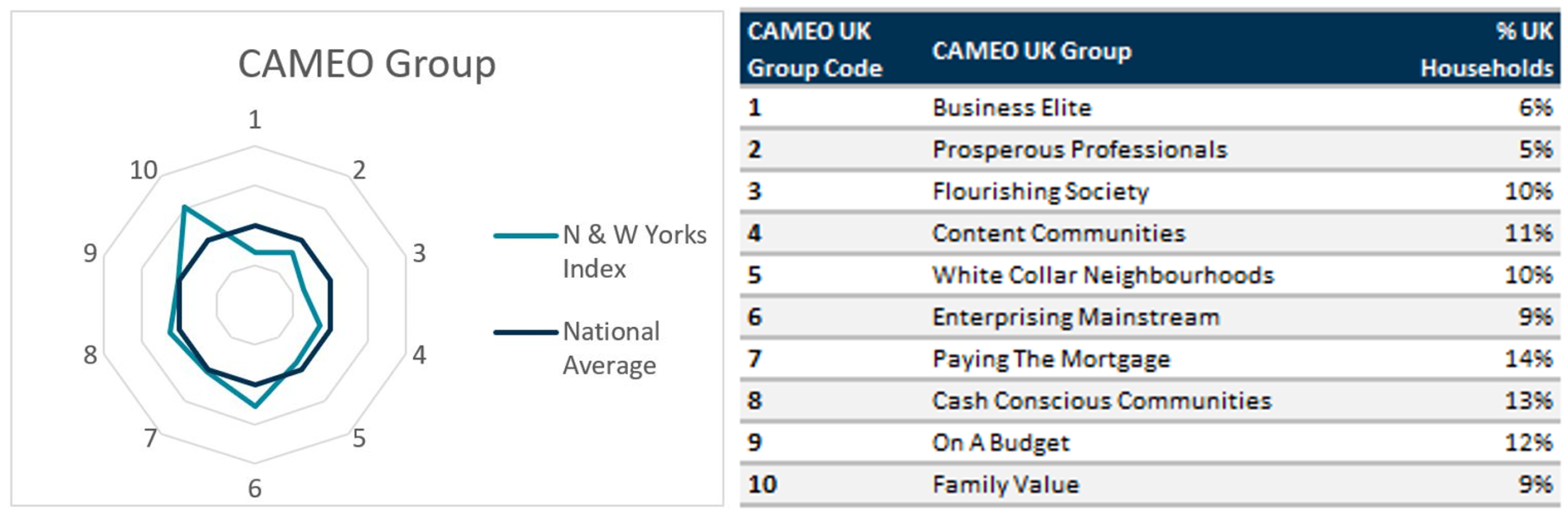

Here at GMAP, we have deployed our MVPLUS interactive mapping system to investigate how feasible cash access is at postcode level, nationally. To do this we ran a proximity analysis to assess the distance between each postcode and the nearest ATM or Post Office, and appended the 2019 CAMEO geodemographic dataset to the results. We then compared the 1.4 million households around our locale within the postcode areas of: Bradford (BD), Huddersfield (HD), Harrogate (HG), Halifax (HX), Leeds (LS), Wakefield (WF) and York (YO) to the national picture.

Although the UK has one of the largest free to use ATM networks in the world, retail banking needs to address the challenge of dispeling public fears over loss of customer service, whilst also making free to use ATMs profitable enough to remain active. As bank branches contiune to shut, banks should see ATMs as an alternative point of contact with their customers. To this end, perhaps the role of the ATM should be re-invented to take on more of the traditional branch based roles, such as 24-hour cash and cheque deposits. Simultaneously, banks should look to spatially re-organise their ATM networks for optimisation. This could prevent further financial exclusion in areas such as Huddersfield, and perhaps reduce the surplus of machines in London.

Studies so far have been undertaken using the geography of Postcode Districts and tend to exclude the location of Post Offices. Postcode Districts are an aggregation of Postcodes, therefore, they have a tendency to mask the intricacies at play. To enable full optimisation and prevent exclusions it is crucial that future studies adopt our methodology and use postcodes as the base geography.

As we have demonstrated in this exploration, GMAP’s MVPLUS system can help you to conduct internal spatial analysis using your own data, CAMEO’s geodemographic segmentation or other data sources. Further insight can be added to your MVPLUS analysis using GMAP’s RetailVision product or DVLA’s anonymised data set . Furthermore, GMAP’s consultancy services, including Ideal Network Plans, Sales Reporting and Bespoke Analysis, can assist you in addressing your industry challenges by providing actionable geographical insights and solutions. Get in touch for more information at info@gmap.com or give us a call at 0113 306 1585

Despite our preference for digital payments, 97% of us carry cash. In fact, the average amount is £41! This culminated in 2.4 billion ATM cash withdrawals in 2018, totalling £193 billion. It is no wonder then that a recent UK public opinion poll concluded only 36% of UK adults believed they could cope with going completely cashless. Government advisors are concerned too. They state eight million UK adults (17% of the UK population) would get left behind – just think about the number of cash-in-hand employments: window cleaners, gardeners, labourers, to name a few. Additionally, consumer association Which? fears that deprived neighbourhoods have the least access to cash, even though they are more dependent on it than their affluent counterparts. Thus, it seems the concerns about the so-called ‘Cash Deserts’ are justified, at least for the next 15 years anyway.

In response, LINK – the network that connects the UK’s cash machines and enables universal access to people’s cash – has set up a £1 million fund to pay for 40 to 50 ATM’s requested by residents in the ‘Cash Deserts’. To qualify as a ‘Cash Desert’, areas must not have access to a free to use ATM or Post Office within 1km and the machine must be in a secure locale.

Here at GMAP, we have deployed our MVPLUS interactive mapping system to investigate how feasible cash access is at postcode level, nationally. To do this we ran a proximity analysis to assess the distance between each postcode and the nearest ATM or Post Office, and appended the 2019 CAMEO geodemographic dataset to the results. We then compared the 1.4 million households around our locale within the postcode areas of: Bradford (BD), Huddersfield (HD), Harrogate (HG), Halifax (HX), Leeds (LS), Wakefield (WF) and York (YO) to the national picture.

Although the UK has one of the largest free to use ATM networks in the world, retail banking needs to address the challenge of dispeling public fears over loss of customer service, whilst also making free to use ATMs profitable enough to remain active. As bank branches contiune to shut, banks should see ATMs as an alternative point of contact with their customers. To this end, perhaps the role of the ATM should be re-invented to take on more of the traditional branch based roles, such as 24-hour cash and cheque deposits. Simultaneously, banks should look to spatially re-organise their ATM networks for optimisation. This could prevent further financial exclusion in areas such as Huddersfield, and perhaps reduce the surplus of machines in London.

Studies so far have been undertaken using the geography of Postcode Districts and tend to exclude the location of Post Offices. Postcode Districts are an aggregation of Postcodes, therefore, they have a tendency to mask the intricacies at play. To enable full optimisation and prevent exclusions it is crucial that future studies adopt our methodology and use postcodes as the base geography.

As we have demonstrated in this exploration, GMAP’s MVPLUS system can help you to conduct internal spatial analysis using your own data, CAMEO’s geodemographic segmentation or other data sources. Further insight can be added to your MVPLUS analysis using GMAP’s RetailVision product or DVLA’s anonymised data set . Furthermore, GMAP’s consultancy services, including Ideal Network Plans, Sales Reporting and Bespoke Analysis, can assist you in addressing your industry challenges by providing actionable geographical insights and solutions. Get in touch for more information at info@gmap.com or give us a call at 0113 306 1585